A company is raising the first $50,000 from an angel investor.

The investor offers to invest in a $4 million Fully Diluted Valuation (FDV).

The founder pauses: does this mean the company is worth $4 million, the future tokens are worth $4 million, or both?

In crypto, you can agree on a valuation in a meeting, but there are different things that need to be sorted out to understand what it actually means.

In this series of posts on valuations, we will break down valuation in crypto deals and learn, in practice, what needs to be defined when you negotiate with your investor, and how to avoid tricks that VCs use to get a lower valuation than what was agreed between the parties.

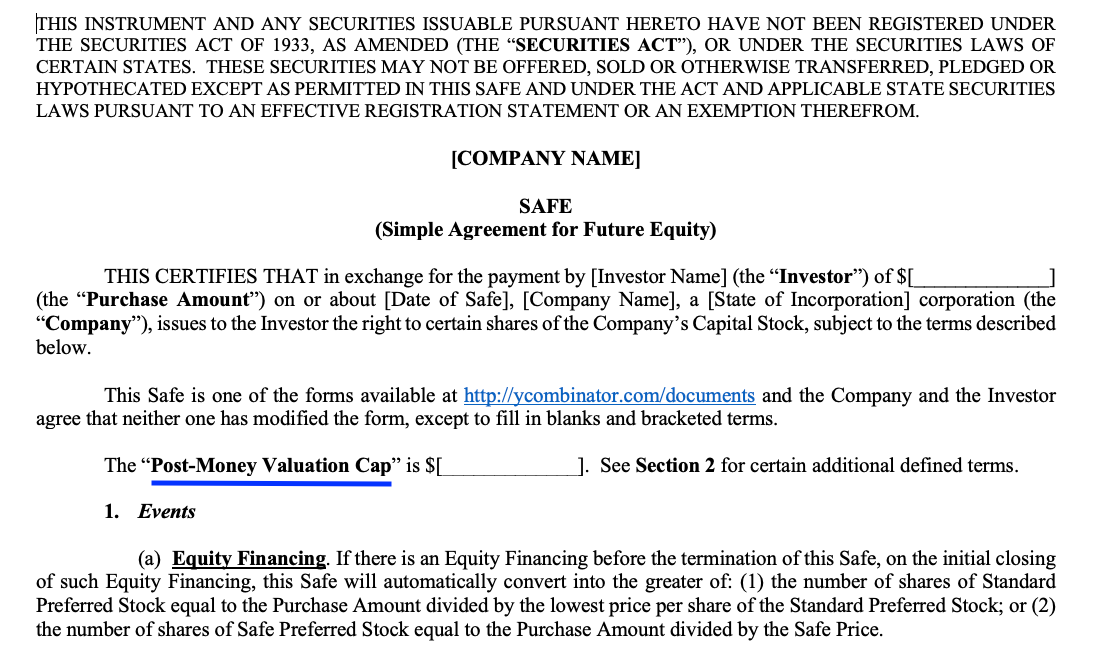

SAFE (Simple Agreement for Future Equity)

A SAFE is a contractual right to receive shares of the company in the future. It is not a debt instrument, which would create interest payment obligations, potential tax issues, and other liabilities for the company as a result of the investor becoming a creditor. It is also not equity itself.

It is important to note that when an investor invests in a SAFE, he is betting on the value of a company: the team, the intellectual property (meaning all knowledge that the employees are creating within the company), and the potential for an acquisition or exit.

When you look at a SAFE agreement, the post-money valuation is shown at the top of the agreement:

SAFT (Simple Agreement for Future Tokens)

Another common investment agreement is SAFT. Instead of receiving equity in the future like with a SAFE, the investor pays now to receive a portion of the network’s future token supply.

Through the SAFT, the investor is valuing the tokens directly, not the company. The investor is valuing the future tokens and thinking about how much they may be worth and for how much he may be able to sell them in the future.

In this case, if the company is acquired, the investor will not be entitled to receive anything from the transaction. As an anecdote, there are times when founders issue SAFTs to investors even without setting up a company.

The valuation of a SAFT agreement is mentioned in different ways. In the example below, you can see that it specifies the percentage of the “Total Token Supply” that the investor will receive. The valuation is calculated as follows: if the investor purchased 1% of the tokens for $50,000, then 100% of the project would imply a $5 million valuation.

Token Warrant / Token Agreement

You may ask yourself: if the investor invests in a SAFE, does he not get exposure to a token?

The answer is no - the SAFE is about the equity. That is why most investors who invest in crypto companies ask for a token warrant or a separate agreement in which the company promises to give the investor tokens if the company issues a token in the future.

Most crypto investors today want a "package deal". They realize that while they are buying equity via a SAFE, the real value may eventually come from a token.

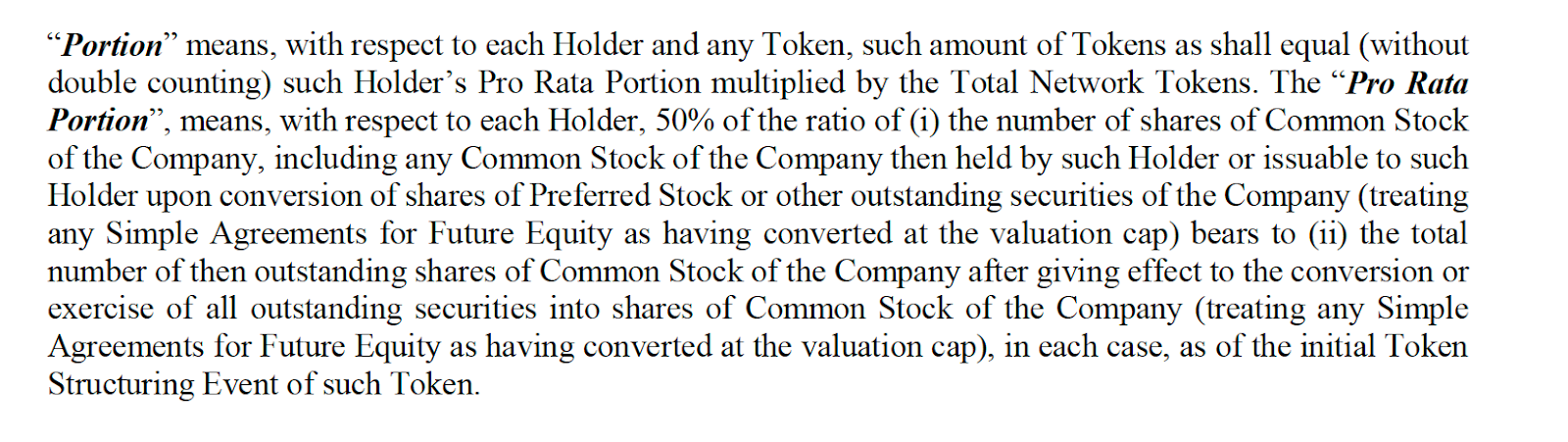

This token warrant or token agreement includes a “token ratio.” The token ratio determines how many tokens the investor gets based on the equity they receive from the SAFE. For example, a ratio of 1:2 means that 1% of equity entitles the investor to 0.5% of the total token supply. You can see the definition of the ratio in the following definition of Portion:

The price of the warrant is relatively low compared to the SAFE, usually a few thousand dollars, and it is essential that the warrant has a price separate from the equity.

Summary

If the agreement is to invest in a SAFT, the valuation refers only to the tokens (the network).

If the agreement is to invest in a SAFE, the valuation refers to equity (the company).

If the agreement is to invest in a SAFE plus a token side letter or token warrant, the valuation refers to both equity and tokens, and an additional amount (usually a few thousand dollars) is allocated for the tokens.